Every month when your credit card statement arrives, you see two numbers side by side: Total Amount Due and Minimum Amount Due. Most cardholders in India understand what the total due is , it is their full bill. But the minimum amount due is misunderstood in a way that is quietly costing millions of Indians thousands of rupees every year.

In this guide, we break down exactly what minimum amount due means, how each major Indian bank calculates it, what RBI rules say, and most importantly — what happens when you keep paying only the minimum. We also cover what competitors don’t: the psychological traps banks use, what options you have when stuck in the minimum-due cycle, and when to seek professional help for ++credit card debt settlement++.

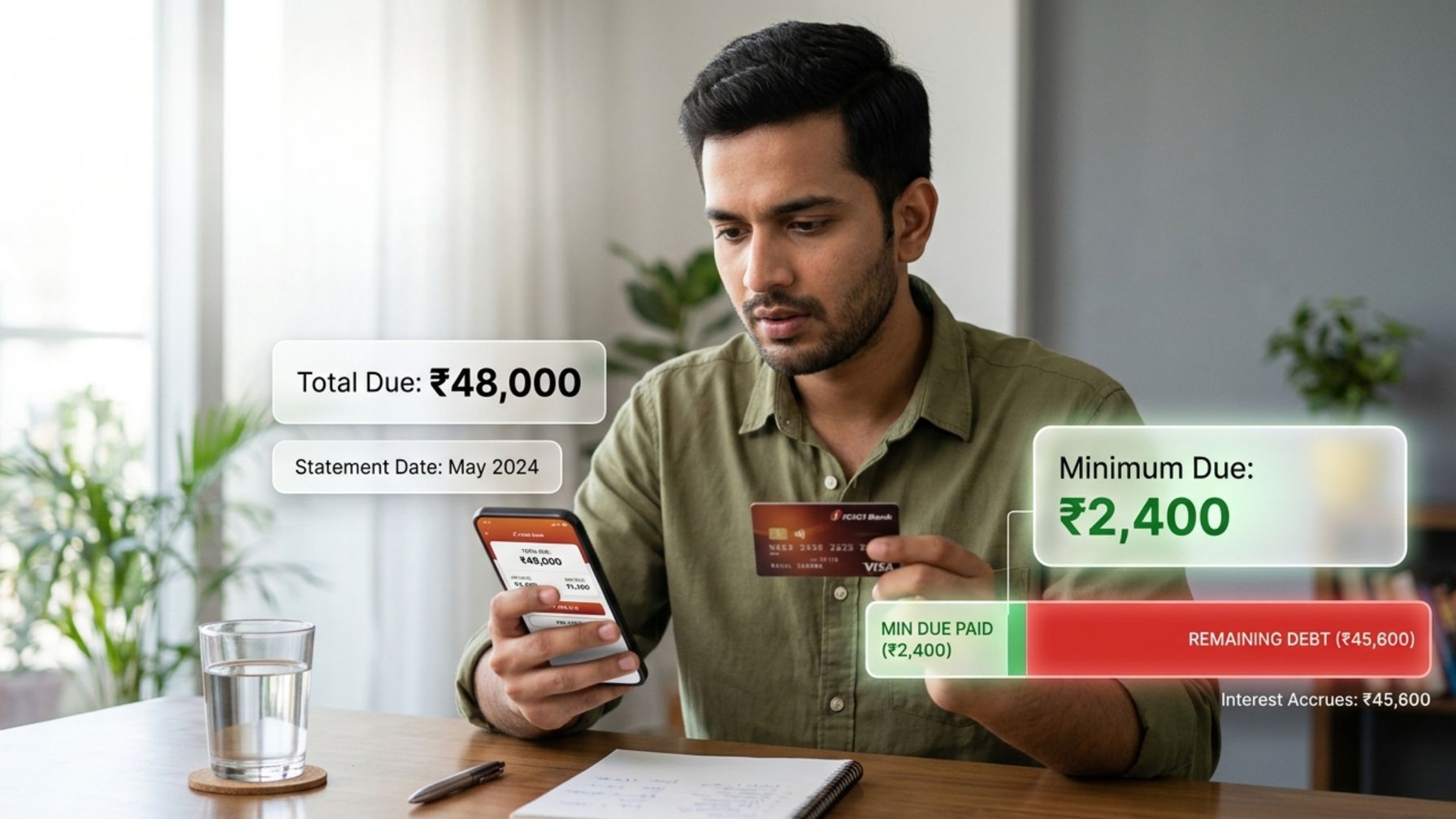

Quick Answer: Minimum Amount Due is typically 5% of your total outstanding balance or Rs 200 — whichever is higher — plus any active EMIs and overdue amounts. Paying it keeps your account active but does NOT stop interest from accruing on the unpaid balance at 30–46% per annum.

1. What is Minimum Amount Due on a Credit Card — Simple Explanation

When your credit card billing cycle ends, your bank generates a statement showing everything you spent that month plus any previous balances. The total amount due is your complete bill. The minimum amount due is the bare minimum the bank will accept by the payment due date to consider your account ‘not delinquent.’

Think of it this way:

• Total Amount Due: Pay this and you owe nothing. No interest charged. Full grace period preserved.

• Minimum Amount Due: Pay this and your account stays active, no late fee — but everything you did not pay rolls over and starts attracting full interest immediately.

The critical point most people miss: The moment you pay only the minimum due instead of the full amount, you lose the interest-free grace period on ALL your purchases — including new ones you make in the next billing cycle. This is one of the most expensive mistakes a credit card holder can make in India.

2. How is Minimum Amount Due Calculated? Bank-wise Breakdown

There is no single RBI-mandated formula. Each bank sets its own method, though the logic is broadly the same across all major Indian banks:

Formula: Minimum Due = 5% of total outstanding + EMI instalments due this month + overdue amounts from previous statements + fees and GST

| Bank | % of Outstanding | Minimum Floor | Notes |

| HDFC Bank | 5% | Rs 200 | EMIs and overdue added on top |

| SBI Card | 5% | Rs 200 | Includes reward redemption dues if any |

| ICICI Bank | 5% | Rs 200 | Fees + GST added separately |

| Axis Bank | 5% | Rs 200 | Same formula as HDFC |

| Kotak Mahindra | 5% | Rs 200 | High-balance accounts may be higher |

| IDFC FIRST Bank | 5% | Rs 100 | Lower floor amount |

| HSBC India | 5–10% | Rs 200 | Higher % for high outstanding balances |

| American Express | 2–5% | Rs 100 | Varies by card variant |

| Yes Bank | 5% | Rs 200 | Standard formula |

| RBL Bank | 5% | Rs 200 | Includes all overdue from prior cycle |

Example Calculation (HDFC Bank)

Your HDFC credit card statement shows:

• Fresh spends this cycle: Rs 40,000

• Previous outstanding: Rs 20,000

• Active EMI instalment due: Rs 3,500

• Late fee from last month: Rs 500 + GST Rs 90

Total Outstanding: Rs 64,090

Minimum Due: 5% of Rs 64,090 = Rs 3,204 + EMI Rs 3,500 + late fee Rs 590 = Rs 7,294

This is why many borrowers are surprised — the minimum due is not simply 5% of what they spent this month.

3. The Grace Period Trap — What Competitors Don’t Fully Explain

Most blogs mention that paying only the minimum due causes interest. What they do not clearly explain is the grace period destruction effect — and it is the most financially damaging consequence.

Here is how it works:

When you pay your total due in full each month, you get an interest-free period of 18–50 days on new purchases (depending on when in the cycle you spend).The moment you pay only the minimum due even once, the grace period is gone for the next billing cycle too.All new purchases you make in the next cycle are charged interest from Day 1 of purchase, not from the due date.This means a Rs 5,000 restaurant bill made 3 days into your new billing cycle starts accruing interest at 3–3.75% per month immediately.

This is the hidden mechanism that makes minimum due payments exponentially more expensive than they appear. Even if you pay the full bill next month, you will still owe interest on the new purchases because you lost the grace period by paying only the minimum this month.

4. The Real Cost of Paying Only Minimum Due — Numbers Indian Banks Don’t Show You

Let us run two real scenarios with Indian bank interest rates.

Scenario A: Rs 50,000 outstanding, SBI Card (3.35%/month = 40.2% p.a.)

| Month | Outstanding (Rs) | Min Due Paid (5%) | Interest Added (Rs) | Remaining (Rs) |

| 1 | 50,000 | 2,500 | 1,593 | 49,093 |

| 3 | 48,200 | 2,410 | 1,534 | 47,324 |

| 6 | 45,700 | 2,285 | 1,455 | 44,870 |

| 12 | 41,500 | 2,075 | 1,322 | 40,747 |

| 24 | 35,100 | 1,755 | 1,118 | 34,463 |

After 24 months of minimum payments: You have paid approximately Rs 51,000 in payments. Your outstanding is still Rs 34,500. Nearly Rs 30,000 went to interest alone.

Scenario B: Rs 1,00,000 outstanding (common for credit card users in metros)

At 3.35%/month, paying only minimum due:

• Time to clear debt fully: 8–10 years

• Total interest paid: Approximately Rs 1,80,000–2,00,000 on a Rs 1,00,000 balance

• Effective cost of that Rs 1,00,000 purchase: Rs 2,80,000–3,00,000

This is not a theoretical scare tactic. These are real calculations using actual Indian bank interest rates. A Rs 1 lakh credit card balance paid only at minimum due can cost you Rs 3 lakh in total repayment.

5. What RBI Says About Minimum Due — Rules Indian Banks Must Follow

RBI’s Master Direction on Credit Cards (updated 2024) includes several protections for borrowers that most competitors do not cover in detail:

- Mandatory Disclosure on Every Statement

Banks must show on every credit card statement: the total amount due, the minimum amount due, and a warning estimating how long it will take to repay the full balance if only the minimum is paid. This was made compulsory under the 2024 update.

- No Interest on Paid Portions

Under a 2023 Supreme Court directive, banks cannot charge interest on the portion of the bill you have already paid. Before this ruling, banks charged interest on the entire billed amount — even if you paid 90% of it. This practice is now prohibited.

- Auto-Debit Must Be Available for Full Amount

RBI mandates that banks must allow customers to set up auto-debit for the total amount due, not just the minimum due. If your bank only offers minimum due auto-pay, you can raise a complaint under RBI’s grievance framework.

Late Fee Slabs (RBI Guidelines)

| Outstanding Amount | Maximum Late Fee Permitted |

| Up to Rs 500 | Rs 0 (no late fee) |

| Rs 500 to Rs 1,000 | Rs 100 |

| Rs 1,001 to Rs 10,000 | Rs 500 |

| Rs 10,001 to Rs 25,000 | Rs 750 |

| Rs 25,001 to Rs 50,000 | Rs 950 |

| Above Rs 50,000 | Rs 1,100–1,300 (bank-specific) |

If you feel your bank has violated any of these rules, you can approach the RBI Banking Ombudsman at bankingombudsman.rbi.org.in. For legal guidance on your rights as a borrower, LawyerPanel provides expert advice on credit card dues and borrower rights.

6. The Psychological Traps Banks Use (What No Competitor Covers)

No mainstream blog explains the deliberate psychological design behind the minimum due concept. Here is what is actually happening:

- The ‘Relief’ Illusion

The minimum due is specifically designed to feel manageable. On a Rs 60,000 bill, a Rs 3,000 minimum due feels like a reasonable payment. Banks know that small, painless numbers encourage you to keep using the card and delay full repayment, which is precisely where they earn the most profit.

- The Anchoring Effect

By displaying the minimum due prominently alongside the total due, banks anchor your perception. Most people instinctively compare the two and feel that paying the minimum is ‘close enough.’ In reality, the gap between paying minimum and paying full is the difference between a one-month bill and a decade of debt.

- The Auto-Pay Trap

Many banks default auto-pay to minimum due when you first set it up. Customers assume their full bill is being paid automatically — and only discover months later that interest has been accumulating. Always verify your auto-pay is set to ‘total amount due’ and confirm with your bank.

- Reward Points as Distraction

Banks promote reward points, cashback, and offers aggressively to encourage spending. High spenders on credit cards are often minimum-due payers — the interest they pay far exceeds any cashback they earn. A 1% cashback on Rs 50,000 spending is Rs 500. The interest on that Rs 50,000 unpaid balance for one month is over Rs 1,500.

Banks earn significantly more from interest on revolving balances than from merchant fees on transactions. The minimum due system is one of the most profitable products in Indian banking — funded almost entirely by borrowers who believe they are managing their finances responsibly.

7. How Minimum Due Payments Impact Your CIBIL Score

Most competitor blogs either oversimplify this or get it wrong. Here is the accurate picture:

| Your Payment Behaviour | Immediate CIBIL Impact | Long-Term CIBIL Impact |

| Pay total due in full | Positive — shows responsible use | Best outcome — low utilisation, clean record |

| Pay minimum due on time | Neutral — no negative entry | Gradual negative — high utilisation ratio reported every month |

| Pay less than minimum due | Negative entry filed with CIBIL | Score drops 50–100 points per missed cycle |

| Miss payment entirely (30+ days) | Delinquency reported to CIBIL | Severe: -100 to -150 points, stays for 7 years |

Credit Utilisation Ratio: This is the ratio of your outstanding balance to your total credit limit. CIBIL considers above 30% high-risk. A person paying only minimum due on a Rs 1,00,000 limit card with Rs 70,000 outstanding has a 70% utilisation ratio — this silently depresses their score month after month even if they never miss a payment.

If you are struggling with rising credit card debt and its impact on your score, read our guide on what happens when you stop paying credit card dues in India to understand the full consequences and your options.

8. Smarter Alternatives to Paying Only Minimum Due

Option 1: EMI Conversion

Most Indian banks allow you to convert your outstanding balance or a large purchase into a fixed EMI plan at 12–18% per annum — dramatically lower than the 30–46% revolving rate. Call your bank’s credit card helpline and ask for ‘balance EMI conversion’ or ‘outstanding EMI on credit card.’

Managing multiple EMIs across different bills? Read smart ways to manage EMI payments for a practical system that helps you stay on top of payment deadlines without defaulting.

Option 2: Balance Transfer

Several Indian banks — including IDFC FIRST, HSBC, and Axis — offer balance transfer schemes where you move your high-interest credit card debt to a new card at 0% for 3–6 months (with a one-time processing fee of 1–2%). This gives you a window to reduce the principal without interest adding up.

Option 3: Personal Loan to Clear Credit Card Debt

A personal loan at 10–16% per annum from your bank is significantly cheaper than revolving credit card interest at 30–46%. If you have a good CIBIL score (700+), you can take a personal loan, pay off the credit card entirely, and repay the loan in structured EMIs at a fraction of the cost.

Option 4: Partial Prepayment Strategy

If you cannot pay the full amount, pay as much above the minimum as possible — every extra rupee reduces the principal on which interest accrues. Even paying 30–40% of the total due instead of just 5% can dramatically cut the time to become debt-free.

Option 5: Request a Hardship Programme

If you are genuinely in financial distress, call your bank and specifically ask for a ‘hardship programme’ or ‘interest rate reduction.’ Banks like HDFC, ICICI, and SBI sometimes offer temporary rate reductions or EMI restructuring for customers who have been with them for several years. Always get any revised terms in writing.

Key Rule of Thumb: If paying only the minimum due is your plan for more than 2 consecutive months, it is time to act — either through EMI conversion, balance transfer, or professional debt resolution assistance.

9. When the Minimum Due Trap Leads to a Debt Settlement Situation

This is the section no competitor covers — because most are either bank-owned platforms or generic finance blogs that do not deal with debt resolution.

There comes a point for some borrowers where:

• The outstanding balance has grown despite months of minimum payments

• Multiple credit cards are all stuck in the minimum-due cycle

• The combined monthly interest exceeds what you can realistically repay

• Banks have begun recovery calls or issued legal notices

At this point, the minimum due is no longer a solution — it is part of the problem. The options available include:

| Option | What It Means | Best For | CIBIL Impact |

| Debt Consolidation Loan | Take one personal loan to clear all card dues | CIBIL 700+, stable income | Neutral — replaces revolving debt with installment debt |

| Credit Card EMI Restructuring | Bank converts dues to fixed EMI internally | Relationship customers | Mild — shows restructuring on report |

| Credit Card Settlement | Negotiate to pay less than outstanding with bank | Severe hardship, cannot repay full | Negative entry for 7 years |

| Professional Debt Resolution | Agency negotiates on your behalf | When bank is unresponsive or amounts are large | Depends on agreement reached |

If you are in this situation, a professional ++credit card debt settlement++ service can negotiate directly with your bank to reduce the outstanding amount, stop interest accumulation, or restructure your repayment into manageable terms.

For a broader perspective on building a financially stable future after resolving credit card debt, read this interview on building a debt-free future in India — practical insights on getting out of the credit card debt cycle for good.

10. Common Mistakes Indian Credit Card Holders Make with Minimum Due

• Treating minimum due as a ‘safe’ payment strategy: It is a short-term lifeline, not a long-term plan. Use it only in genuine emergencies.

• Setting auto-pay to minimum due and forgetting: Check your auto-pay settings. Many banks default to minimum due at setup.

• Not accounting for EMIs in minimum due: If you have converted purchases to EMIs, those add to your minimum due. Many borrowers are surprised by a higher-than-expected minimum payment.

• Continuing to spend while in minimum-due mode: Every new purchase loses the grace period benefit and starts accruing interest from day one.

• Ignoring credit utilisation: Even with no missed payments, consistently carrying 70–80% utilisation slowly damages your CIBIL score.

• Waiting too long before seeking help: The longer you pay only the minimum, the more the principal grows through interest. Early action always leaves more options.

11. Step-by-Step: How to Get Out of the Minimum Due Trap in India

Calculate your exact total outstanding across all credit cardsCheck your CIBIL score — this determines which options are available to youContact your bank and ask for **EMI conversion on outstanding balance** — this is the fastest, cheapest first stepIf you have multiple cards, prioritise the one with the highest interest rate first (debt avalanche method)If your CIBIL is 700+, explore a **personal loan or balance transfer** to consolidate all card dues at a lower interest rate10. Set up auto-pay for at least the total amount due on your primary card to prevent future minimum-due cycles

- If you are already in legal recovery or cannot sustain any repayment plan, contact a ++credit card debt settlement++ professional immediately

One month of paying only the minimum due is a financial inconvenience. One year of it is a debt trap. Three years of it is a crisis. The time to act is always now.

12. Conclusion

The minimum amount due on a credit card is one of the most misunderstood — and most financially damaging — concepts in Indian personal finance. It is not a repayment strategy. It is a floor designed to keep your account active while the bank earns maximum interest on your outstanding balance.

If you are currently paying only the minimum due, the smartest move you can make today is to stop treating it as a plan and start treating it as an alarm. Explore EMI conversion, balance transfers, or — if the situation has already escalated — professional ++credit card debt settlement++. For expert legal guidance on your credit card borrower rights, LawyerPanel is a trusted resource for Indian borrowers.

The path to becoming debt-free starts with one decision: to pay more than the minimum. To understand what that journey looks like, read this real-world feature on building a debt-free future in India.

Remember: Every rupee you pay above the minimum due is a rupee that does not generate 40% annual interest for the bank.